Macroeconomic indicators were published earlier this week and further showed the continuation of the US economic recovery. The business activity in the manufacturing sector is growing again, according to Markit in June. While PMI increased from 54.6p to 55.4p, the ISM index showed an increase to 60.2p against 58.7p, but a slight decrease was projected not growth. In May, the of production volume orders increased by 0.5%, and the overall impression indicates that growth of the dollar in recent months is based on the Fed's exit from the soft monetary policy as well as on the recovery of the US manufacturing sector, which Trump is directly seeking.

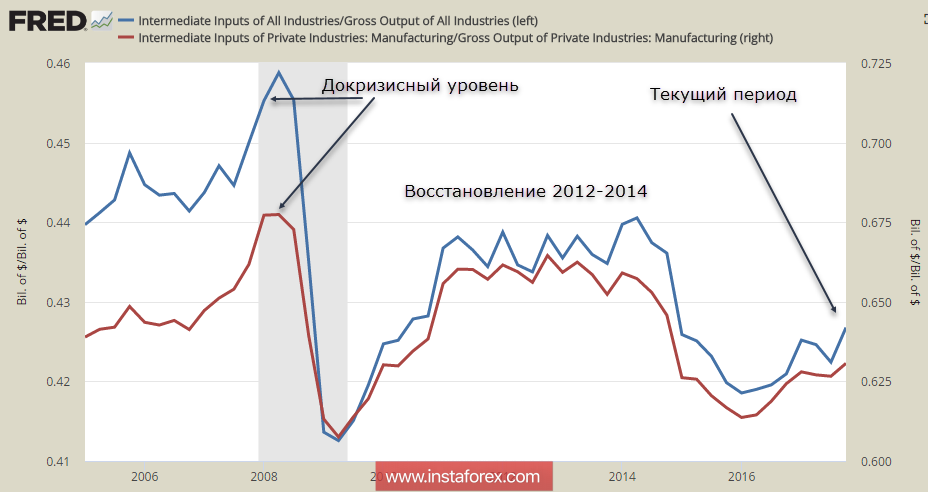

At the same time, an in-depth look at the recovery prospects shows that not everything is as good as it may seem. Let's consider the dynamics of so-called "goods of a production cycle", which are used for manufacture of final production. For example, when assessing the pace of construction, it is possible to take into account the dynamics of the total finished houses, as well as the volumes of demand for cement, brick, glass, etc. As clearly shown from the graph below, the ratio of costs for intermediate goods to the total output for all sectors of industry remains lower than in the pre-crisis level, and also lower than the recovery period in 2012-2014, when no one had ever thought about leaving incentive programs. A similar scenario is expected for a particular private sector.

Despite the strong growth in business activity, the US manufacturing sector in fact remains quite far from recovering.

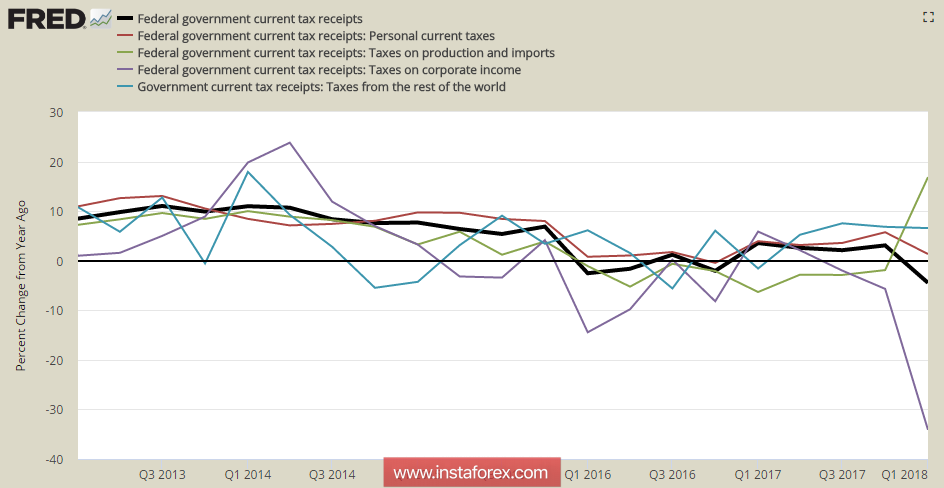

The second component which you need to pay attention is the government's revenues after the launch of the tax reform. We have already paid attention to the estimate of the Congressional Budget Committee, which was forced to revise upward the expenditure side for the next decade, while the profitable one - to the downside, noting the inevitable growth of the budget deficit.

The initial data results for reforms showed that the trend is negative. According to the results of the first quarter, the revenues growth was shown based from increased of excises and imports. Here, we see the result of the gradual recovery of the manufacturing sector. At the same time, corporate tax revenues collapsed by 35%, in general, the dynamics are negative and the government is forced to dramatically increase borrowing to finance the budget.

There are no ways to dramatically increase budget revenues through private consumption, as there is no way to significantly reduce costs to offset the balance. In order to reverse, or at least smooth out the trend, the government should consistently insist on protectionism for its own producers, and change the trading conditions in its favor.

We see another confirmation that protectionism and trade wars are the consequence for the development of negative trends in the US economy, and not the personal whim of the president. There is no reason to believe that the US can make concessions in trade disputes with China or the European Union.

Thus, the most likely scenario for the development of the situation on world markets after July 6 is the escalation and growing tension. These factors will objectively raise the demand for defensive assets, in particular, for yen, gold and the US dollar.

Other significant events of the week are the Fed's minutes publication for the June 13 meeting and the labor market report. The minutes should be hawkish since the speech of the FEd members has become more aggressive generally, which led to an increase in the forecast rates. However, these factors have already been taken into account in the current quotes. If investors see a hint about the possible easing of the Fed's position, then this may lead to some dollar weakening for the week, if not - the dollar will react with a slight increase.

While the labor market report showed fears that the labor demand by the companies has somewhat decreased, as indicated by the PMI data in May. However, both ISM and Markit reported again the activity growth on Monday, therefore, non-farm payroll would likely exceed its forecasts, which will support the dollar.

Thus, the dollar may begin to strengthen again by the end of the week. The EUR/USD pair will check for strength at 1.15, while the GBP/USD pair may go below 1.30, and the yen will fall below 110.

* The presented market analysis is informative and does not constitute a guide to the transaction.