The Fed unanimously kept the range of the key rate at 1.25 - 1.50% at the meeting on Wednesday. The results of the meeting did not lead to increased volatility since they fully corresponded to the forecasts.

The tone of the accompanying statement can be considered moderately optimistic. The Fed expects inflation to rise this year along with a moderate economic growth, based on its expectations on employment growth and household spending.

Thus, the last meeting under the leadership of Janet Yellen was planned and without surprises. The new chairman, Jerome Powell, was unanimously elected and will take office on February 3.

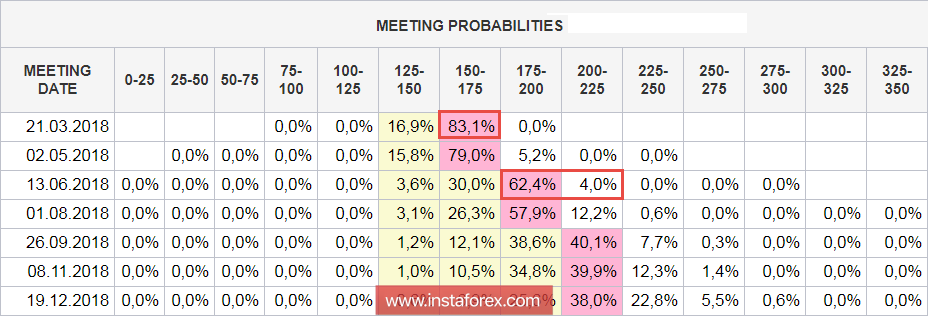

Markets are convinced that the rate will be increased by a quarter of percent in March. The probability of this event, according to the data of the CME futures market, is 83.1% as of today. Moreover, the second increase this year will take place in June with respect to the third and last opinion which has not yet formed. This means roughly equal chances for September and December.

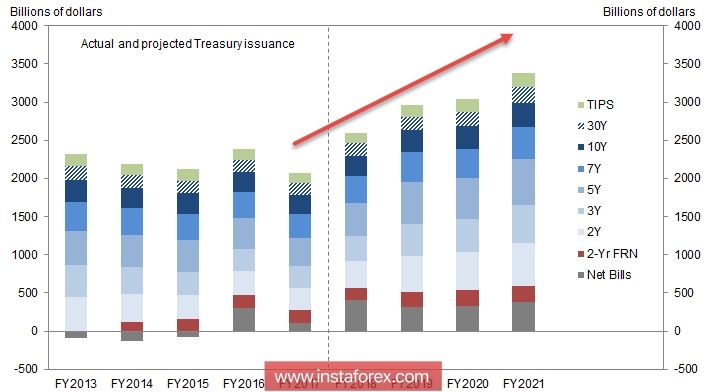

However, after all, raising rates on the background of lowering the tax rate will increase the burden on the budget as the government's interest payments will grow. Illusions are not present. The forecasted requirements of the US government for the current fiscal year will be 1.03 trillion. The budget deficit in 2018 will be 0.75 trillion (3.7% of GDP) and in 2019 1.05 trillion (5% of GDP). The Ministry of Finance intends to attract 441 billion dollars until the end of the first quarter. In the second quarter they aim to get another 176 billion which will lead to an increase in the national debt to June 21.1 trillion dollars.

Until recently, the main buyer of the debt was the Fed. However, the policy of reducing the balance is aimed at stopping the practice of reinvestment and reduce the balance of the Fed in excess of 2 trillion. This has been announced since November last year. In the first quarter, the Fed will reduce its portfolio of treasuries by 36 billion. In the second quarter, it will reduce by 54 billion. Mortgage bonds are also guaranteed by the government to be planned out of balance.

Who will be the main buyer of US debt in the coming years? The answer to this question is the main intrigue at the moment.

New investors should focus on outrunning growth in yields and lowering bond prices and current holders. On the contrary, lower prices are useless. Consequently, we are seeing the beginning of the process of changing the composition of the holders of the US national debt but it is still unclear to whom the role of paying the banquet is for.

The strategy of attracting foreign capital fits the logic of a weakening dollar since it will reduce the costs of foreign borrowers. The depreciation of the dollar is also beneficial to the government of Trump as it will give exporters an edge and increase the chances of winning the beginning currency wars with the main US trading partners.

Thus, the forecast is confirmed about the US dollar currently not having internal reasons for the resumption of growth. The need to correct the trade balance, maintain a course for re-industrialization, and, at the same time, ensure a faster growth in the yields of Treasury bonds while reducing the collection of taxes, leave neither the Trump administration nor the Fed any other choice than to adhere to the current line of weakening the dollar.

The Fed predicts an increase in inflation by the end of this year but the internal reasons for its growth are too weak. Growth in personal consumption expenditure in December was only 0.1%. For the year, growth was at 1.7%, which is lower than the November 1.8%, and without rising costs, inflation can not be increased. At the same time, the example of inflation in the UK shows that growth of up to 3% was obtained solely due to expensive imports caused by the depreciation of the pound.

Today, we need to pay attention to the ISM index in the manufacturing sector. Some decrease is expected which will put pressure on the dollar. Tomorrow, the report on the labor market in January will show optimistic forecasts. The market expects the growth of new jobs to 175 thousand and the growth of average wages to 2.6%. These expectations are already included in the quotes but the dollar, however, did not react to growth.

By the end of the week, the dollar index may fall. The favorites are European currencies, primarily the euro and the franc.