Global macro overview for 03/07/2017:

It might be a busy trading week, so let's take a look at the top events in the economic calendar this week. It might start slowly, mainly due to the US Independence Day holiday, but it will get very interesting at the end of the trading week.

Monday, 03/07/2017:

The new quarter will start with the floods of PMI reports from the leading economies in the world. We will begin with Japan, South Korea, China, India, Russia, and Turkey, followed by Holland, Poland, Spain, Italy, France, Germany, the Eurozone, the United Kingdom and the US. On this occasion, it is worth recalling that in the last report the German PMI won again.

At 09:00 am GMT the Eurostat will present data on the condition of the EU labor market.

It is worth remembering that July 3 is a special day for Americans because of the national holiday on July 4th. So, on Monday the Wall Street session will last until 05:00 pm GMT.

Tuesday, 04/07/2017:

The Independence Day celebrated in the US is associated with the lack of trading activity in the local stock and bond markets. The absence of American traders will also be visible on the trading floors of the whole world, so the volatility will be limited.

Besides, it is hard not to find important events, only interest rates will be decided by the Reserve Bank of Australia (04:30 am GMT) and Riksbank of Sweden (07:30 am GMT), while Eurostat will announce PPI from the Eurozone (11:00 am GMT).

Wednesday, 05/07/2017:

Traditionally, two days after the PMI Manufacturing sector index review, it will be time to publish the corresponding indexes for the PMI Services sector. We will look at the situation in Japan, Russia, Spain, Italy, France, Germany, the Eurozone, and the UK. At 09:00 am GMT Eurostat will present data on May Retail Sales in the Eurozone.

US Mortgage Applications (11:00 am GMT) and Factory Orders (02:00 pm GMT) will be published during the US trading session. More important than this publication will be the content of the minutes of the last meeting of the Federal Open Market Committee (06:00 pm GMT), during which a decision was made to increase interest rates. Investors will, as always, seek to find in the document guidelines for future Federal Reserve's moves. The last accent of the day will be a notice of change of oil reserves (09:40 pm GMT) from EIA.

Thursday, 06/07/2017:

We will begin with the next report from the German economy (Factory orders, 06:00 am GMT), which has nothing but all positive signals in recent weeks. At 07:15 am GMT we will be able to get acquainted with the dynamics of inflation in Switzerland and at 11:15 am GMT with the most important event of the day - minutes of the meeting of the European Central Bank.

In the US, the countdown begins on Friday's Non-Farm Payrolls publication. Thursday's Challenger and ADP reports will be available on the market at 11:30 am GMT and 02:15 pm GMT respectively. A little later, the market will find information on the number of claims for unemployment benefits (02:30 pm GMT) and US Trade Balance data (02:30 pm GMT). The rest of the day in the US will be the service sector's report (PMI at 01.45 pm GMT, ISM Non-Manufacturing PMI at 04:00 pm GMT).

Friday, 07/07/2017:

The data for Industrial Production in Germany, France, Spain, and the UK will be released in the morning. In addition, reports on foreign trade will appear on both sides of the English Channel (Trade Balance data from France at 06.45am GMT, for the UK at 08:30 am GMT).

The most important publication of the day will, of course, be the June report from the US labor market, which will see the light of day at 12:30 pm GMT. According to economists, the Non-Farm Payrolls should deliver an increase in employment by a solid 180 thousand against a weak May reading of 138 thousand (as usual, possible revisions). It is also worthwhile to look at wage dynamics (+ 0.3% m/m increase is expected), because of the prospects for further rates increases by the Fed.

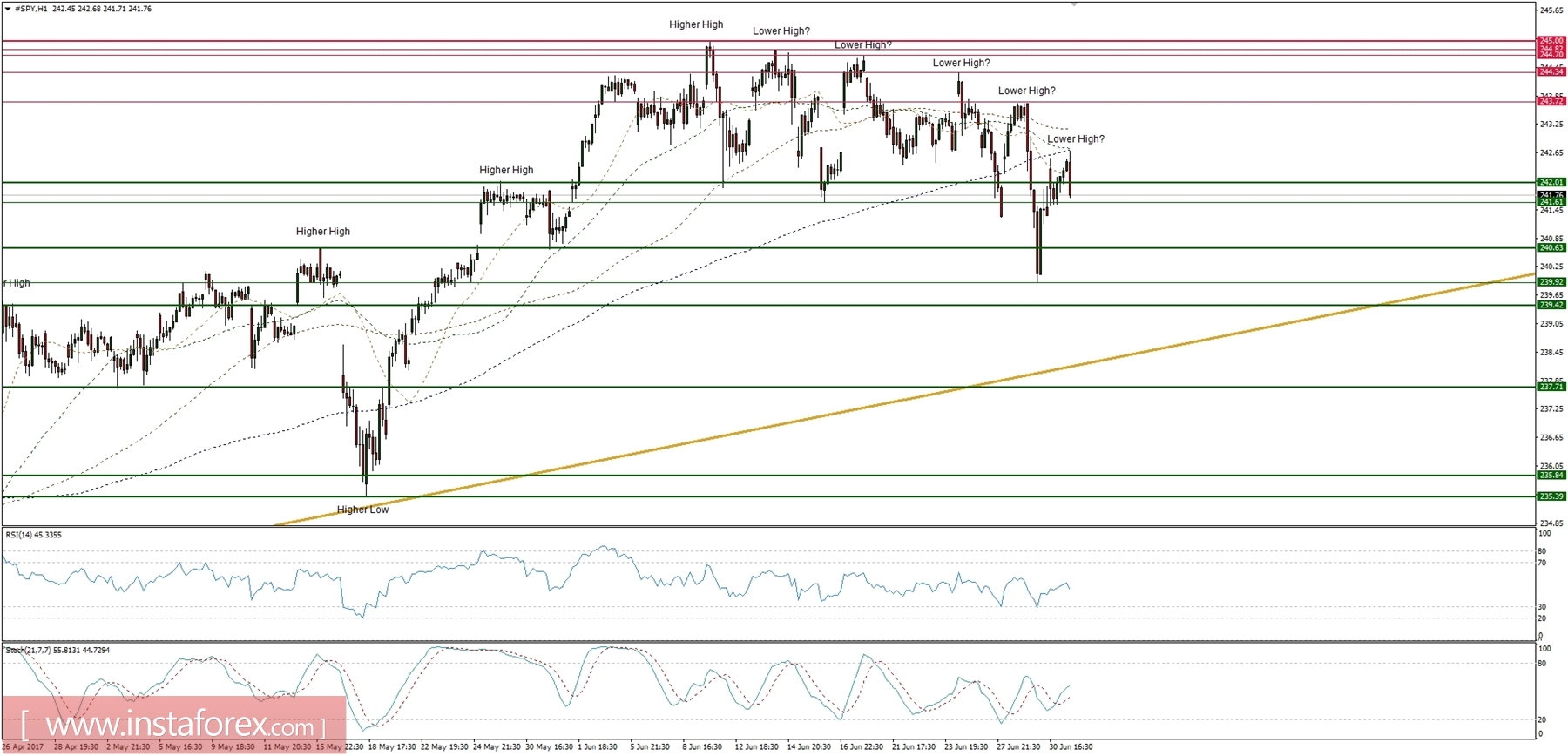

Because the whole week is all about the US data release, let's now take a look at the US stock index, the SPY (SP500 ETF) technical picture on the H1 time frame. The price has tested the recent highs at the level of 245.00 three times and it failed to break out higher so far. The series of five lower highs is clearly visible on the hourly time frame chart, so the odds for a further slide towards the next technical support at the level of 239.92 is possible. Nevertheless, as long as the technical support at the level of 235.39 is not violated, the overall bias remains to the upside.